On January 11, 2026, the Department of Justice served the Federal Reserve with subpoenas, threatening criminal indictment related to the testimony of Fed Chair Jerome Powell before the Senate Banking Committee in June 2025 regarding a multi-year project to reconstruct historic Fed office buildings costing $2.5 billion.

The actions of the Donald Trump administration are a tool to enhance the manageability of the Fed and reduce its ability to block Washington’s broader geoeconomic priorities.

This involves the desire to transform the Fed from a semi-autonomous institution into one whose actions are synchronized with the White House’s financial diplomacy and the architecture of control over global trade chains.

In this construct, the Fed’s monetary policy must align with the administration’s goals of reformatting global markets and strengthening the dollar’s role in the world economy.

The White House strategy relies on reprogramming global trade and energy circuits so that they once again work for the dollar infrastructure. The priority is restoring transactional demand for the dollar through control over market access rules.

In this model, the dollar regains strength as a currency of access, where entry into legitimate global markets is increasingly tied to dollar procedures, U.S. licenses, and compliance with sanctions regimes.

Over the previous years, international trade in oil and gas has gradually lost its strict dollar dependence due to the growth of bilateral settlements in national currencies, experiments with alternative payment systems, and coordination of efforts by China, Russia, and BRICS countries to reduce the dollar’s role in strategic sectors.

The Venezuela case became a turning point in this trajectory, demonstrating that access to global energy markets is once again being built around U.S.-controlled dollar infrastructure, and the sanctions and licensing mechanism is used to forcibly re-tie exports to American currency jurisdiction.

This approach directly strikes at the strategic positions of China and the BRICS coalition, which viewed energy de-dollarization as a tool to weaken U.S. financial influence, since the return of the dollar to the center of energy settlements automatically restores demand for American financial assets and strengthens Washington’s global monetary leverage.

In such a configuration, the Trump administration needs increased manageability of the Fed, as the effectiveness of the petrodollar directly depends on synchronizing monetary policy with foreign economic and sanctions instruments, and the Fed’s autonomous position with a tight rate begins to be perceived as a factor limiting U.S. strategic mobility in global financial competition.

In addition, the Department of Justice’s investigation into the Fed’s building reconstruction is part of a broader ecosystem of economic pressure decisions, within which the Trump administration is trying to address public demand for a change in monetary policy by undermining the authority of the Fed as an autonomous decision-making center.

Washington uses the legal investigation as a tool of public pressure on monetary policy, embedding in public consciousness the causal link between the Fed’s high policy rate, rising credit costs, and the deterioration of households’ financial situation.

This logic is aimed at the institutional model of the Fed, which is perceived as an autonomous decision-making center with limited sensitivity to the social consequences of its own policy, allowing the administration to intensify criticism of the tight monetary line without launching a formal procedure to review the Fed’s mandate.

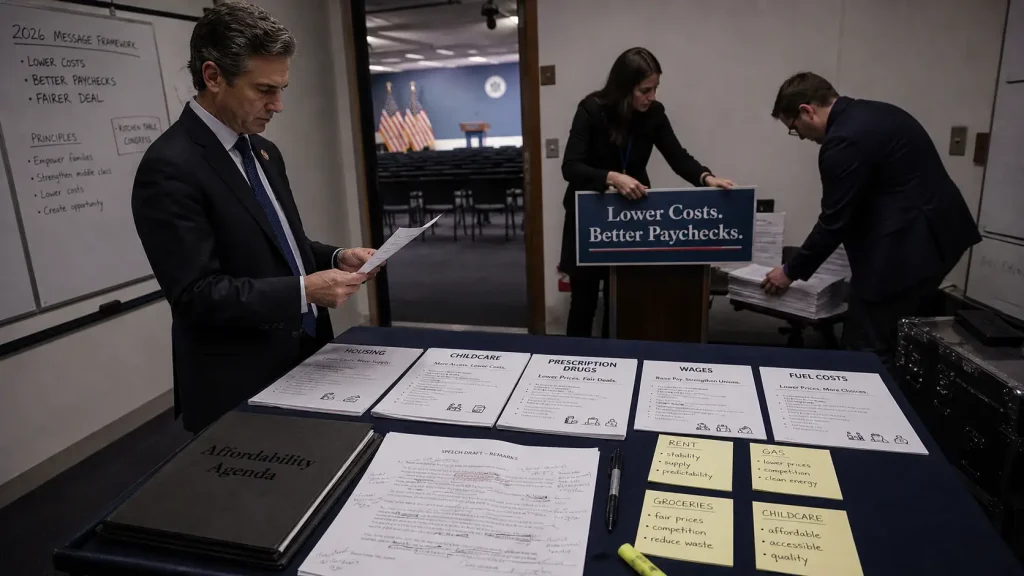

That is why, in parallel, the White House is deploying a package of quasi-fiscal decisions in the housing sector, where the use of pension savings, restrictions on institutional investors, and interventions by Fannie Mae and Freddie Mac form a contour of compensation for the middle class without formally lowering the rate.

Thus, on January 8, 2026, President Trump stated that he had instructed the two major government mortgage finance companies, Fannie Mae and Freddie Mac, to begin purchasing mortgage-backed securities.

Following this statement, the spread between interest rates on mortgage bonds and Treasury bonds narrowed, which is a sharp shift in this market and the first sign that this initiative may have some impact on the mortgage market.

Also, the day before, on January 7, U.S. President Donald Trump stated that he intends to prohibit large corporate investors from buying single-family homes to make housing more affordable for Americans.

Trump stated that he would ask Congress to “codify” this plan and discuss it at the World Economic Forum in Davos at the end of January 2026.

This promise reinforced an idea that has been circulating for years among housing advocates and lawmakers in response to Wall Street’s growing role in the U.S. residential real estate market. However, some analysts question how much the ban will affect prices.

These tools signal to the market that the U.S. is ready to directly influence mortgage costs, compressing the spread between Treasuries and mortgage rates by 0.1%, and at the same time demonstrate to the electorate in the midterm elections the political will to act beyond traditional monetary orthodoxy.

The Trump administration’s initiative to allow the use of pension savings for down payments on housing fits into a broader strategy of reorienting the U.S. financial system from macro-level stability to micro-level household liquidity, where access to housing becomes a key political indicator of economic well-being.

The proposed logic, voiced by Kevin Hassett, shifts pension savings from a passive long-term savings tool to a hybrid financial asset that simultaneously works in the housing market and the private pension system, blurring the classic boundary between consumption, investment, and social security.

Essentially, the White House is offering Americans to compensate for the deficit of affordable credit through the mobilization of their own capital, substituting the problem of high mortgage rates with a mechanism of internal redistribution of savings, which allows avoiding direct confrontation with financial markets and the Fed at the regulatory level.

This approach removes political responsibility for the structural inaccessibility of housing from monetary policy and shifts it to individual financial decisions of citizens, while creating the illusion of expanding opportunities without immediately lowering credit costs or correcting real estate prices.

In the strategic dimension, the initiative signals a change in state priorities: future pension stability gives way to the political necessity of stabilizing the current standard of living in the U.S., especially ahead of election cycles, where homeownership remains one of the few material markers of middle-class economic success.

Housing affordability, including high mortgage rates and limited access to affordable housing, remained one of the main concerns of voters during the 2024 presidential elections.

The situation showed that economic markers of living well-being directly influence political sentiments and determine electoral priorities.

A Pew Research Center survey found that 69% of Americans were “very concerned” about housing costs, while at the beginning of 2023 this figure was 61%, making housing affordability a central election issue.

A Redfin analysis showed that 53% of owners and renters believed that the housing problem directly influenced their choice in the elections, emphasizing how much the political importance of this issue has grown in a short period.

In their campaigns, both Donald Trump and Kamala Harris paid special attention to the housing issue. Harris proposed tax incentives to create 3 million new homes and support first-time buyers, while Trump focused on limiting the participation of large institutional investors and stimulating the middle class through government mortgage interventions.

Both strategies were aimed at compensating for the deficit of about 7 million affordable housing units that had accumulated due to slowed construction.

Mortgage rates in the election year remained volatile due to policy uncertainty, and after the 2024 presidential elections, 30-year fixed rates slightly decreased from 6.79% to 6.69% over the month.

High rates only deepened the housing affordability problem, leaving many potential buyers out of the market and underscoring the political necessity of government intervention to stabilize household financial conditions.

In this sense, pressure on the Fed serves as an accelerator of expectations and demonstrates that even without an immediate decision to lower the Fed’s policy rate, the market begins to price in future easing, which lowers long-term interest benchmarks for housing lending.

The context of the midterm elections in this regard is not reduced to mobilizing the electoral base, but to attempting to reprogram the priorities of the American, who increasingly reacts less to ideological markers and more clearly evaluates power through mortgage payments and housing accessibility.

The shift in values, recorded by the Wall Street survey, creates a window of opportunity for the administration, where economic pragmatism displaces symbolic politics, and reducing financial pressure on households becomes the main currency of political loyalty.

For the Fed, this means losing its monopoly on interpreting stability, as stability in political discourse is increasingly equated with the ability to service debt, buy housing, and maintain purchasing power, rather than with inflation reduction goals.

In the short-term perspective, such a configuration increases the likelihood of a gradual rate cut or at least a change in the Fed’s rhetoric, as further ignoring political pressure risks turning institutional independence into a factor of electoral destabilization.

In this logic, the discussion about the “weakness of the dollar” becomes a continuation of internal monetary tension, as the decline in the dollar’s share in global reserves and the dollar’s fall in 2025 are read by markets through the prism of expectations of future political intervention in U.S. policy rate reduction.

The public narrative about the dollar losing its status as a “safe haven” serves as a tool of pressure on the Fed, as the administration uses devaluation expectations to legitimize the need for cheaper money in the household economy.

The dollar’s paradox lies in the fact that amid record pessimism from investment houses and loud statements about collapse, it is precisely the concentration of short bets against the American currency that forms conditions for sharp counter-movements, which manifested in the strong start of the dollar index (DXY) at the beginning of 2026.

The Fed in this situation records a fundamentally different reality, where despite reserve diversification, the dollar maintains dominance in international settlements, and control over energy contracts turns into a tool for supporting transactional demand without direct appeal to reserve status.

Embedding Venezuelan energy rents into American legal and financial contours restores the classic logic of the dollar as a trade currency, not a symbol of trust, reducing the significance of reserve statistics for the real functioning of currency infrastructure.

The rise of gold to historical highs after news of pressure on the Fed reflects not flight from the dollar, but fear of politicization of monetary decisions, when markets begin to hedge against the scenario of losing predictability in central bank actions.

Simultaneous large-scale liquidity injections by the Fed through the “overnight repo” mechanism at the end of 2025 in more than $16 billion signal that the Fed maintains control over financial stability, and the record drop in volatility in the Treasury market indicates the absence of systemic panic despite the aggressive political background.

At the same time, the weak labor market at the end of 2025 consolidates the “no-hire, no-fire” model, where formal stability hides the exhaustion of income dynamics, pushing households to support any decisions capable of reducing debt burden.

In the end, fluctuations in the dollar index, turbulence around the Fed, and stagnation in the labor market converge into a single political construct, where the Trump administration seeks to manage expectations through control of household credit costs, even at the expense of long-term risks to monetary stability.

It is in this configuration that pressure on the central bank, devaluation narratives, and quasi-fiscal interventions form a managed regime of instability, in which the key asset becomes not market trust, but voter loyalty, measured by the monthly mortgage payment.

In the end, this forms a unified architecture of managed easing, where formal independence of monetary policy gradually gives way to the political economy of household stability.

The global context only amplifies this trajectory: in 2025, G10 countries’ central banks cumulatively cut policy rates by 850 basis points, which became the largest easing cycle since 2009 and a clear signal of the end of the era of tight anti-inflation regimes.

For the U.S., this creates a convenient external backdrop, within which a potential Fed rate cut would appear not as a concession to political pressure, but as synchronization with the global trend of normalizing monetary conditions after the global energy shock of 2022.

In the short-term perspective, this increases the likelihood of a soft pivot in the Fed’s rhetoric already in 2026, with gradual lowering of long-term rates and compression of credit spreads even in the absence of sharp decisions on the federal rate.