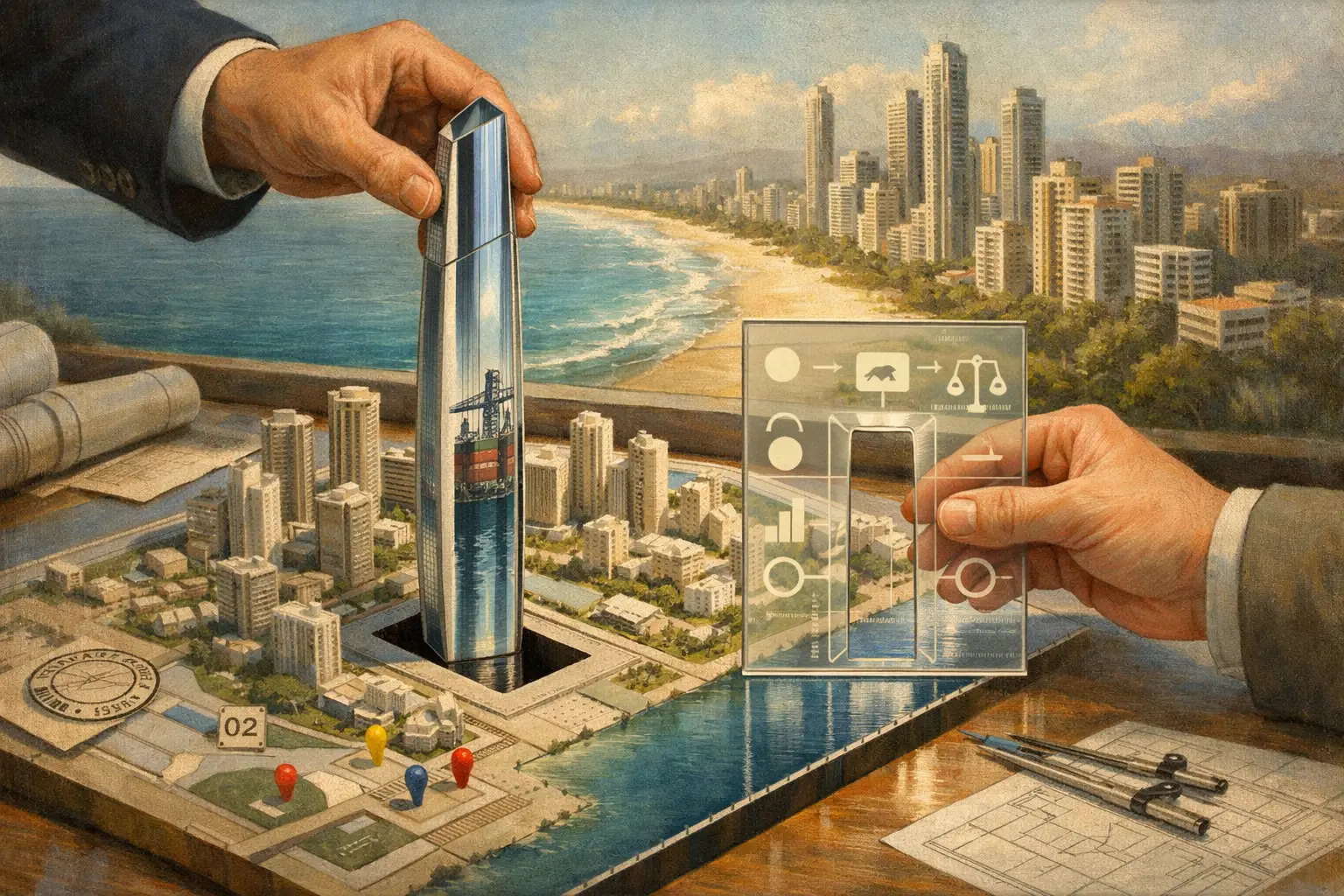

On January 15, 2026, sources in local authorities on Australia’s Surfers Paradise coast reported that Donald Trump is considering acquiring “abandoned” real estate with an approximate value of $65 million on this coast for the construction of a super-tower Trump Tower.

The Trump Tower project on Surfers Paradise fits into Australia’s strategy of selective openness, under which the state prioritizes allied American capital, while limiting China’s participation in investment projects in the commercial real estate sector.

The Australian state systematically views real estate in tourist and coastal zones as an element of space control, where control over land, services, and communication with local communities shapes social and cultural patterns that extend far beyond financial indicators.

After a series of problematic cases with Chinese developers, Canberra shifted from balanced regulation to active selection of investors, where the key criterion became not the scale of capital, but its strategic origin, transparency, and political compatibility with the Australian model of state governance.

This experience allowed Australia to form a strict but predictable filtering system, in which Chinese capital retains access to trade and exports, but faces restrictions in the commercial real estate sector that shapes long-term spatial and social presence.

Institutionally, this is reinforced by enhanced control from the FIRB (Foreign Investment Review Board) and the Australian Taxation Office (ATO).

Under these rules, the share of foreign ownership in commercial real estate consistently remains below 30%, and residential real estate owned by foreigners is limited to approximately 40,000 properties, mostly acquired by Chinese investors before the tightening of the regime after 2016.

Within this filtering system, access to coastal assets ceased to be neutral, and restrictions for Chinese developers were combined with targeted admission of allied American capital, including projects associated with the Trump brand, which is perceived as politically compatible and manageable within Australian regulatory frameworks.

Thus, the failure of the Chinese Forise project on Surfers Paradise in 2015 became an element of policy in which regulatory requirements, financial pressure, and public wariness became a mechanism for displacing Chinese capital from sensitive assets.

The blocking of Chinese investments worth $1.2 billion on Surfers Paradise became the result of Australia’s accumulated institutional experience, when the state shifted from situational decisions to systemic filtering of capital based on criteria of strategic and social sensitivity of assets.

The Forise Investment Australia case unfolded during a period when Chinese capital was actively buying up Australian real estate, using complex corporate structures, lending from mainland China, and politically vulnerable municipal approval mechanisms.

The acquisition of the site on Surfers Paradise occurred under conditions of a relatively soft regulatory regime, but already at the implementation stage, the state faced opacity in funding sources, dependence on Chinese banks, and instability in the developer’s cash flows.

Financial problems of Fu Hua Group, creditor lawsuits, and failure to fulfill basic obligations to Australian regulators became for Canberra confirmation of the risks associated with Chinese developers, whose business model relied on politically controlled lending.

In parallel, public and political reaction to the role of Chinese donors in the project approval process intensified, including suspicions of influence on decisions by the Gold Coast City Council, which prompted a review of practices for interacting with foreign developers.

At the federal level, this coincided with the strengthening of FIRB (Foreign Investment Review Board) powers, which began to interpret China’s investments in real estate and other assets as assets with potential impact on national security, social stability, and the information environment.

A key factor in blocking investments from China and other countries was the understanding that large residential-hotel complexes create a permanent presence of foreign personnel, service networks, and cultural practices, forming alternative channels of China’s influence in Australia.

After freezing the Forise project, the state de facto blocked its revival through Chinese refinancing, using regulatory checks, requirements for capital sources, and delays in approvals as tools of strategic containment.

The sale of the site to a consortium from Macau and Hong Kong after blocking the deal with a Chinese company did not lead to the resumption of construction, which only solidified Canberra’s position on the undesirability of returning Chinese influence to this location even in an indirect form.

As a result, the Surfers Paradise region turned into a demonstrative example of controlled cleansing of space from Chinese developer capital without formal bans, but through the accumulation of financial, regulatory, and political barriers.

It is under these circumstances that the vacuum that arose in the market became accessible to allied capital, where the investor’s origin matters more than its financial capabilities, and strategic compatibility in terms of values and state governance, as in Australia-US, becomes a priority.

This mechanism demonstrates that Australia has learned to block unwanted Chinese presence not through direct confrontation, but through risk management, procedures, and time, transforming regulation into a tool of long-term geopolitical selection.

Canberra demonstrates readiness to accept China as a key buyer of raw materials, energy carriers, and agricultural products, maintaining trade balance, while limiting access to sectors that create physical and cultural presence through housing, hotels, and urban space.

Thus, the volume of trade between Australia and the US in 2025 amounted to $57.7 billion (US exports to Australia: $31 billion, and Australia’s exports to the US: $26.7 billion), while the volume of trade between Australia and China in 2025 is $177 billion (312 billion Australian dollars).

Washington, in turn, uses private investment brands as a form of soft institutional expansion that allows consolidating influence in allied jurisdictions without formal state intervention and political toxicity.

For Australia, such a format of relations with the US and the Trump company is comfortable, as it moves in parallel with the strengthening of US-Australia cooperation within AUKUS and mineral agreements while preserving autonomy in regulatory policy toward foreign investors.

The contrast between the Chinese model of aggressive entry into real estate and the American model of “branded” capital shows that for Canberra, the origin of investments is important as a marker of strategic trust.

It is particularly telling that this concerns a location with already approved development parameters, where the state chooses who exactly will fill the permitted space, determining the future social ecosystem of the district.

In this sense, Trump Tower functions as a geo-economic filter that screens out Chinese expansion in symbolic zones, leaving Beijing the role of a trade partner without the right to shape urban environments and political views of the local population through everyday communications.

Despite preserving China’s status as Australia’s largest trade partner, Canberra clearly signals that economic interdependence does not transform into spatial or cultural interpenetration.

Thus, the Australian strategy demonstrates a containment model where trade serves as a tool of pragmatic benefit, and control over land and real estate—as a tool of long-term geopolitical hygiene amid growing rivalry with China.

In such a configuration, real estate, tourism, and logistics hubs transform into tools for fixing the political orientation of states, as they create long-term physical presence and channels of social interaction.

In the medium-term perspective, this means that for China, trade in cheap goods will become the only tool for preserving influence in global trade, while it will increasingly encounter restrictions in areas that shape cultural presence and local communities.

For the US, such evolution opens the possibility of consolidating influence without direct confrontation, using brands, family capital, and allied jurisdictions as elements of an expanded geo-economic strategy.

In summary, the Australian real estate project reflects that investments cease to be neutral, the territory of a state or its islands becomes an object of strategic selection, and the future architecture of influence is built through control over land, services, and daily interaction between investors and local representatives.